One Community

One Community

Taxes and Sustainable Community Building

This page will continuously develop to share the details of sustainable community building tax-related processes and the details of One Community’s tax process specifics. It includes what we annually file for our nonprofit, what we’ll need to file for any for-profit activities, and other sustainable community tax-related resources.

We discuss these areas with the following sections:

- What are Open Source Tax Processes

- Why Open Source Tax Processes

- Taxes and Community Building

- Becoming a Nonprofit

- Taxes Nonprofits Still Have to Pay

- How to Set Yourself Up to be Transparent

- One Community Tax Specifics

- Resources

- Summary

- FAQ

NOTE: The content of this page is from our research and work completed by industry professionals. We will continuously update this page with our experience but you should still have a professional of your own check your tax compliance and details.

RELATED PAGES (mouse-over icons for descriptions, click for complete pages)

")

")

")

")

")

")

CLICK THESE ICONS TO JOIN US THROUGH SOCIAL MEDIA

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

WAYS TO CONTRIBUTE TO EVOLVING THIS SUSTAINABILITY COMPONENT WITH US

SUGGESTIONS ● CONSULTING ● MEMBERSHIP ● OTHER OPTIONS

CONSULTANTS ON THIS TAX GUIDE

Binru Chen: Accountant Specializing in Audit and Financial Reporting

Lucy Lu: Accountant Specializing in Financial Reporting and Managerial Accounting

WHAT ARE OPEN SOURCE TAX PROCESSES

Open source tax processes are the complete tax processes we’ve researched for operating a sustainable community as a business entity. One Community is a nonprofit 501(c)(3) organization, but we’ve also included here for-profit tax details. As One Community continues to develop, builds the Duplicable City Center and each of the 7 villages, and launches and maintains our revenue streams, we will continuously update this page to share all the specifics of our tax processes and ongoing considerations.

Open source tax processes are the complete tax processes we’ve researched for operating a sustainable community as a business entity. One Community is a nonprofit 501(c)(3) organization, but we’ve also included here for-profit tax details. As One Community continues to develop, builds the Duplicable City Center and each of the 7 villages, and launches and maintains our revenue streams, we will continuously update this page to share all the specifics of our tax processes and ongoing considerations.

NONPROFIT ANNUAL TAX PROCESS

Here is One Community’s annual nonprofit tax responsibilities and process:

Here is One Community’s annual nonprofit tax responsibilities and process:

CLICK HERE FOR OUR NONPROFIT-FORMATION TUTORIAL

- Pay registered agent service ($49 through online service) and File Annual Report

- Wait for email confirmation

- Log into registered agent and download the Annual Report/Renewal Notice

- File Annual Report with the state. Click here for a resource showing when this is needed for each state.

- Visit state division of corporations and use a credit card to renew business (Due 3/31 for us) – paying $10 (+$3 fraud protection) to process your renewal using the Entity # and Renewal ID # found on the notice downloaded in #2

- Save a screenshot of your payment confirmation (you will also (immediately) receive an email confirmation)

- File Form 990-N if gross receipts are under $50,000 (The e-Postcard is due every year by the 15th day of the 5th month after the close of your tax year – May 15 for us because our tax year closes Dec 31st.)

- If you’ve logged in before, no need to create a new account

- Once you fill out the information, take a screenshot of your completion confirmation that will say: Congratulations, your Form 990-N (e-Postcard) has been submitted to the IRS. Once the IRS receives and processes your e-Postcard (usually within 30 minutes), you will receive an email indicating whether your e-Postcard was accepted or rejected. If accepted, you are done for the year. If rejected, the e-filing receipt email will contain instructions on how to correct the problem.

FOR-PROFIT ANNUAL TAX PROCESS

If One Community were a for-profit business, this would be our tax process:

If One Community were a for-profit business, this would be our tax process:

CLICK HERE TO LEARN HOW TO FILE AN EXTENSION IF MORE TIME IS NEEDED

NOTE: These may be needed for non-profit also.

- File Statement of Information with the state ($25)

- File quarterly payroll tax returns (Due: 4/30, 7/31, 10/31, and 1/31)

- In CA: Pay S-Corp fee with CA Form 100-ES to the (CA) Franchise Tax Board: $800 (Due April 15th)

- Request and print year-end summary(s) for company credit card(s)

- Use a spreadsheet to sort expenses into categories. Here are the ones we use:

- Supplies

- Salary

- Payroll Taxes

- Auto

- Bank Charges

- Consultant Fees

- Donations

- Dues and Subscriptions

- Education

- Insurance

- Internet

- Meals & Entertainment

- Office Supplies

- Office Equipment

- Outside Service

- Postage

- Printing

- Professional Fees

- Promotions

- Rent

- Supplies

- Telephone

- Travel

- Depreciation

- Penalty

- Taxes/Licenses

- Use Tax

- Franchise Tax Board Tax

- Use a spreadsheet to sort expenses into categories. Here are the ones we use:

- Print year-end summary for company bank account

- Highlight all checks paid

- Research and label who all the payees were

- Send 1099 forms (www.irs.gov/form1099misc) to all who were paid over $600 during the year (Due 1/31)

- File top 1099 form (Copy A) with Form 1096 (www.irs.gov/form1096) – address to mail to is on this form

- Mail 3rd 1099 form (Copy C) to recipients

- File all other forms in a “Taxes 20xx” File

- Itemize all income

- Pay state and federal income taxes (Due March 15th)

- Pay estimated taxes if filing an extension (Taxes then due September 15)

WHY OPEN SOURCE TAX PROCESSES

One Community is meant to function effectively as either (or both) a for-profit and nonprofit entity. Open sourcing our experience and research into both tax processes and other tax considerations related to community setup is purposed to teach people what to consider before starting and exactly what each process entails. This is so people can make more educated decisions about what kind(s) of entity(s) they wish to set up and where might be the best places to start a community if land hasn’t been purchased yet.

One Community is meant to function effectively as either (or both) a for-profit and nonprofit entity. Open sourcing our experience and research into both tax processes and other tax considerations related to community setup is purposed to teach people what to consider before starting and exactly what each process entails. This is so people can make more educated decisions about what kind(s) of entity(s) they wish to set up and where might be the best places to start a community if land hasn’t been purchased yet.

TAXES AND COMMUNITY BUILDING

Taxes should be considered when beginning any community building project. Early consideration is important because taxes are different in different countries, different states, and different counties. This page is focused on the US (for now), and purposed to help people find the information they need as part of their US development process and/or their state and county selection process.

The following areas are discussed:

- Tax Considerations State-by-State

- Department of State Taxation Web Pages

- Tax Considerations Community by Community

- Tax Considerations of Nonprofit vs. For-profit

TAX CONSIDERATIONS STATE BY STATE

The best way to understand taxes for a specific area is to talk to a tax specialist within that area. There are resources though that can help you to have a basic understanding of the tax differences for various areas. Here are a few examples showing these tax differences between different states and counties. How important these differences are will differ greatly based on the goals and financial structure of your own community. Here are a few examples to put the differences in perspective:

STATE TAXATION COMPARISONS

/about/state-income-tax-rates-2-2014-tax-foundation-57a631e35f9b58974a3ad3a4.png "Click to Enlarge")

.png)

County by County Average Property Tax Comparison – Click Image for Interactive Tool

DEPARTMENT OF TAXATION WEB PAGES

To review the most current details for each state and access the state-specific tax documents, here are links to each state’s government tax page. If you are just beginning to consider a location, and you don’t know what state you want to build in, we suggest reading this entire page before beginning any state-specific research. This will help you to better understand what you are looking for.

TAX CONSIDERATIONS COMMUNITY BY COMMUNITY

So, what are the tax concerns that you need to be aware of if you are starting a community? To answer this question, it is helpful to think of your community as a business because “businesses” are what the tax code was written for. With this in mind, many aspects of a business influence the amount of tax due, and even the slightest change of the daily operation can result in hundreds of dollars in tax savings or wasting. This number can balloon to thousands, tens of thousands, or even more if your business/community becomes large enough.

Here are some factors that you might want to be aware of during tax planning:

- Business Mission: The mission of the business is what determines whether the company is a for-profit (FP) or not-for-profit (NFP) organization. FP company’s missions are to increase shareholders’ equity, and NFP business’ missions are to improve the well being of society, which is usually a responsibility of the government. Because of this, local governments grant tax benefits to NFP organizations.

- Property: The purpose, owner, or the market value of the property also influences the taxes due. Actual rates vary among states, usually between 0% to 4% of the property value. When an organization uses the property, either owned by the organization or leased from a third party, for specific NFP reasons, such as education, charity, hospital, etc. they can take a full or partial property tax exemption. If the entire property is used for NFP reasons, they will receive full exemption If only a portion of it is used for the above purposes, they will receive partial exemption. Companies can apply the tax benefit by submitting the Tax Exemption Application to the State Tax Commission. Click here for the step by step tutorial

- Employees: NFP organizations may be exempt from some federal taxes, but they are subject to employee taxes, which include Social Security tax and Medicare tax (also known as hospital insurance tax). For reference, in 2015 the tax rate for Social Security was 6.2% for the employee and 6.2% for the employer on the first $118,500 of the wages. The tax rate for Medicare was 1.45% for the employee and 1.45% for the employer on the full/complete employee wages. Click here for the current tax rates

- Location: Each state or city has its own taxation rules, please refer to the state web pages above for state specifics. Do your research first if you have the flexibility to begin your community in any location you choose.

TAX CONSIDERATIONS OF NONPROFIT VERSUS FOR-PROFIT

Another consideration when forming any collaborative community is whether to operate as a for-profit, nonprofit, neither, or both. There are significant differences between the taxation of for-profit and non-profit entities. Operating as “neither” would mean that the community is just a group of people living together and not having any specific entity structure.

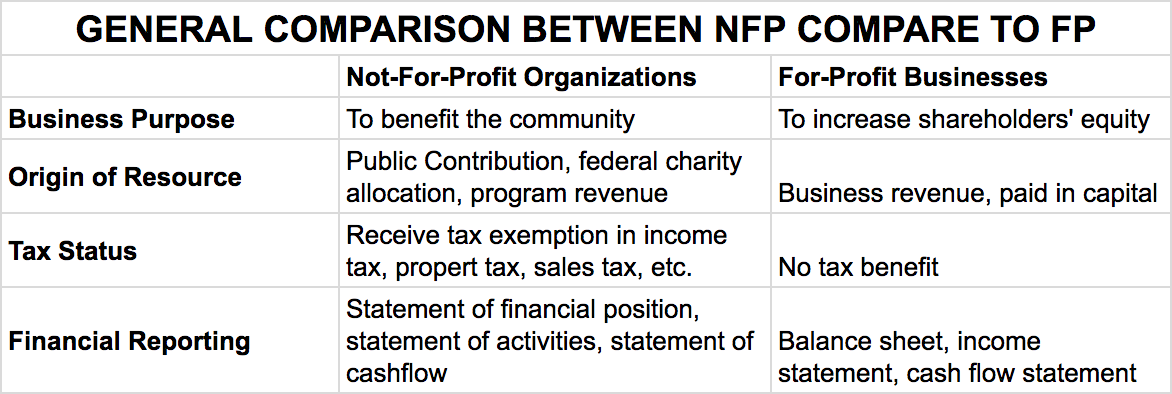

Here is a general comparison between a nonprofit and for-profit entity:

Here is a side-by-side comparison of the taxation rule differences between a nonprofit (NFP) organization and a for-profit (FP) business:

PROPERTY TAXES

Property tax consideration includes location, purpose, and market value. A NFP organization might be exempt from the property tax if the whole property is used for qualified purposes. The insurance expense and coverage on the property varies. If the property is owned and managed by the company, the insurance can cover both the building and the office content. But if the property is leased from a third party, the insurance can only cover the office content.

SALES AND INCOME TAX

NFP organization who received tax exempt status will not be subject to sales tax and income tax, which can be huge savings for the company. However, the sales tax exemption is only valid on purchases of necessities used in qualified activities. For example, when hospitals make purchases of medicines, it will qualify as a necessary product and will be free of sales tax, but if they buy shavers to sell in the pharmacy store, this purchase will be considered unnecessary and thus will not receive the tax benefit. Similar rules apply to income tax exemptions, only the portion of income that is directly related to the qualified activities will be tax free.

EMPLOYEE TAXES

Employee taxes include Social Security tax and Medicare tax. The tax rate changes every year and it is calculated by multiplying a certain percentage with the employee wages. The employee tax rates are the same for NFP and FP companies. For organizations that hire unpaid volunteers, the employee taxes will be greatly reduced because the wages are considerably lower than for-profit businesses.

Click here for everything One Community filed to receive our 501(c)3 nonprofit status

BECOMING A NONPROFIT

Initially, One Community thought that some aspects of One Community’s revenue generating ventures like eco-tourism, sale of products, etc. would only be able to be operated as for-profit. Thanks to the help of our tax and accounting consultants, we’ve now come to believe that all aspects of One Community can be part of our nonprofit. Any that aren’t will be covered with complete details on our for-profit page.

For organizations like ours that are seeking to operate as 100% nonprofit, here are the steps you need to get started:

NOT-FOR-PROFIT ORGANIZATION EXEMPTION CRITERIA

As we’ve already discussed, classifying your organization as nonprofit has significant tax benefits. However, to classify any revenue generating venture as not-for-profit, you must satisfy several key criteria:

As we’ve already discussed, classifying your organization as nonprofit has significant tax benefits. However, to classify any revenue generating venture as not-for-profit, you must satisfy several key criteria:

- It must be exclusively for exempt purposes as set forth in the 501(c)(3) application and maintenance criteria (see below). There is also a “Distribution Constraint.” This means that surplus income cannot be distributed to organizational Directors (or equivalent) as dividends.

- It must be “member serving or community serving.” This means the venture should benefit a particular group of people (ex: credit unions or sports clubs) or provide services to the community in general (ex: educational service or medical research) or both.

- Your organization as a whole must meet the 501(c)(3) organization requirements: (click here for the IRS page about this)

- Exclusively for exempt purposes set forth in 501(c)(3)

- May not be an “action organization” (attempt to influence legislation or participate in campaign activities for or against political candidates, etc.)

- Must not be for private interests, and no part of the earnings may inure to any private shareholders or individual(s)

If an organization fulfills the standards above, it can file Form 1023 to the IRS to apply for recognition of exemption under Section 501(c)(3). Section 501(a) focuses on other nonprofit or tax-exempt organizations. The qualified organizations under Section 501(a) can file Form 1024 to the IRS to apply for recognition of exemption.

HOW TO APPLY FOR TAX EXEMPTION STATUS

Here are the steps you can expect when applying for tax exemption status. To help understand the paperwork, you can also click here for copies of everything we filed when we applied for our nonprofit status.

Here are the steps you can expect when applying for tax exemption status. To help understand the paperwork, you can also click here for copies of everything we filed when we applied for our nonprofit status.

- Determine the right category. Will you be a Private Foundation or a Public Charity? A Private Foundation has a single major source of funding and is the default category for most organizations. A Public Charity receives funding from multiple sources, including the general public

- Request an Employer Identification Number (EIN). This must be done even if the organization does not have any employees. You use application form SS-4 to request your EIN: http://www.irs.gov/pub/irs-pdf/fss4.pdf

- Submit the application (Form 1023-series) for exempt status under section 501(c)(3). Here is what you’ll need:

-

- Standard application in PDF (Form 1023): http://www.irs.gov/pub/irs-pdf/f1023.pdf

- Interactive version with hints and links (Form 1023, interactive): http://www.stayexempt.irs.gov/Starting-Out/Interactive-Form-1023-Prerequisite-Questions

- Streamlined e-filing for smaller NFP (Form 1023-EZ): Organizations who meet all the requirement specified in Form 1023-EZ eligibility worksheet (http://www.irs.gov/pub/irs-pdf/i1023ez.pdf ) will be able to apply the exempt status through Form 1023-EZ: http://www.irs.gov/uac/About-Form-1023EZ

- This e-filing method requires simpler supporting documents and will significantly reduce the process time

- We paid LegalZoom to help with all our paperwork, which can be found here

-

- Include the user fees for your exempt organization. The amount of user fees varies, you can use this link to find one that matches your organization: http://www.irs.gov/irb/2017-01_IRB/ar11.html#d0e18567

- Double check you have everything ready. Here is a step-by-step review to use to double check your work: http://www.irs.gov/Charities-Non-Profits/Application-Process

- Submit the complete application portfolio to the Internal Revenue Service (IRS)

- Public inspection after receiving the tax exemption. The organization needs to have its approved application with all supporting documents and last three annual reports ready at all times for public inspection.

Additional Note: If you intend to apply for 501(c)(3) status, you must notify the Internal Revenue Service within 27 months from the date of formation if you desire to be treated as a 501(c)(3) from the date formed.

NONPROFIT ANNUAL REPORTING AND FILING

The IRS requires tax exempt organizations to file annual returns. There are some exceptions, click here for details. Here is an overview of what is required.

- The forms to be filed as annual return depends on the nonprofit’s financial activities

- File Form 990-N for organizations whose gross receipts are normally < $50,000. (Most small tax-exempt organizations whose annual gross receipts are normally $50,000 or less are required to electronically submit Form 990-N, also known as the e-Postcard, unless they choose to file a complete Form 990 or Form 990-EZ instead).

- File Form 990-EZ or Form 990 for organizations whose gross receipts are <$200,000 and total assets are <$500,000.

- File Form 990 for organizations whose gross receipts are >$20,000, or total assets are >$500,000.

- File Form 990-PF for private foundation, regardless of financial status.

DUE DATES FOR NONPROFIT ANNUAL RETURNS

The initial return date is the 15th day of the fifth month after the organization’s ending date of tax year, the first extended due date is the 15th day of the eighth month after the organization’s ending date of tax year, and the second extended due date is the 15th day of the eleventh month after the organization’s ending date of tax year.

For example, an organization’s ending date of tax year is December 31, its initial return date would be May 15th, the first extended return date would be Aug. 15th, and the second extended return date is November 15th.

If a due date is not on a business day, the due date is delayed until the next business day.

PUNISHMENT FOR FAILURE TO FILE AN ANNUAL RETURN

According to section 6033(j) of the Internal Revenue Code, organizations that do not file for three consecutive years automatically lose their exempt status. An automatic revocation is effective on the original filing due date of the third annual return or notice.

The IRS posts the list of organizations which fail to file an annual return for three consecutive years. These organizations are no longer exempt from federal income tax. Consequently, they may be required to file Form 1120 or Form 1041 and pay applicable income taxes. Furthermore, these organizations are not eligible to receive tax-deductible contributions and will be removed from the cumulative list of tax-exempt organizations provided by the IRS.

However, these organizations have opportunities to reinstate their tax-exempt status in four different ways. You can read more about this here.

TAXES NONPROFITS STILL HAVE TO PAY

There are still some taxes nonprofits have to pay. We discuss these here:

- Employment Tax

- Unrelated Business Income Tax (UBIT)

- Property Taxes

- Miscellaneous

EMPLOYMENT TAX

If the non-profit organization has employees, they must still withhold employment taxes from their employee’s wages. The employment taxes include federal income tax withholding (FITW), social security and Medicare taxes (FICA), and federal unemployment taxes (FUTA). This is the same as for-profit businesses.

In general, the organization (employer) must deposit federal income tax withheld, and both the employer and employee social security and Medicare taxes. The organization has to decide which deposit schedule to use, monthly or semiweekly, before each calendar year. Reviewing Publication 15 for Forms 941, 944 and 945, or Publication 51 for Form 943 can help the organization determine the payment schedule. A maximum penalty is up to 15% if the organization doesn’t make a timely deposit.

There is a base limitation for Social Security tax, which means the organizations withhold their employee’s gross wages until they reach an annual base limit, and employee’s wages above the limit are not subject to social security tax.

However, all wages are subject to the Medicare taxes.

- To report employer’s quarterly federal tax return, use Form 941.

- FUTA is only paid by the non-profit organization, and employees don’t have to pay for it.

- An organization that is exempt from income tax under section 501(c)(3) of the Internal Revenue Code is also exempt from FUTA. An organization that is not a section 501(c)(3) organization is not exempt from paying FUTA tax.

- To report employer’s annual federal unemployment (FUTA) tax return, use Form 940.

- If a person services a non-profit organization as an independent contractor, the organization does not generally have to withhold or pay any taxes on payments to him/her.

- To differentiate employee and independent contractor, you can find more information using this link http://www.irs.gov/pub/irs-pdf/p15a.pdf.

EMPLOYMENT TAX FORMS

| Form I-9 | Employment Eligibility Verification |

| Form SS-4 | Application for Employer Identification Number |

| Form SS-8 | Determination of Worker Status |

| Form W-2 | Wage and Tax Statement |

| Form W-2C | Corrected Wage and Tax Statement |

| Form W-3 | Transmittal of Wage and Tax Statements |

| Form W-3C | Transmittal of Corrected Wage and Tax Statements |

| Form W-4 | Employee’s Withholding Allowance Certificate |

| Form W-4P | Withholding Certificate for Pension or Annuity Payments |

| Form 940 | Employer’s Annual Federal Unemployment Tax Return |

| Form 941 | Employer’s Quarterly Federal Tax Return |

| Form 941 | Schedule B, Employer’s Record of Federal Tax Liability |

| Form 941-X | Adjusted Employer’s QUARTERLY Federal Tax Return or Claim for Refund |

| Form 943 | Employer’s Annual Tax Return for Agricultural Employees |

| Form 944 | Employer’s Annual Federal Tax Return |

| Form 945 | Annual Return of Withheld Federal Income Tax |

| Form 1040ES | Estimated Tax for Individuals |

| Form 1040 | Schedule H, Household Employment Taxes |

| Form 1042 | Annual Withholding Tax Return for U.S. Source Income of Foreign Persons |

| Form 1099-MISC | Miscellaneous Income |

| Form 1099-R | Distributions from Pensions, Annuities, Retirement or Profit-Sharing Plans, IRA, Insurance Contracts |

| Form 1120 | U.S. Corporation Income Tax Return |

| Form 4137 | Social Security and Medicare Tax on Unreported Tip Income |

| Form 8027 | Employer’s Annual Information Return of Tip Income and Allocated Tips |

UNRELATED BUSINESS INCOME TAX (UBIT)

Unrelated Business Income Tax (UBIT) is another tax nonprofits still need to pay. Determining your UBIT liability can be accomplished using the following 4 steps:

Step One: determine if your organization engages in unrelated business activities.

Tax exempt non-profit organizations may engage in trade or business activities. If these trade or business activities regularly occur and are not substantially related to the organization’s tax-exempt purpose, income produced by these business activities is subject to Unrelated Business Income Tax (UBIT).

Step Two: determine if your organization’s business activities fall into the categories below.

Unrelated business activities include sale of merchandise and publications, advertising, gaming, rental income, parking lots, and debt management plan service.

- Sale of Merchandise and Publications: If a non-profit organization sells merchandise, publications or any other things not related to the exempt purpose of the organization, the income from business activities above will be subject to tax.

- Advertising: This may include the sale of advertising space in bulletins, magazines, and journals, or on the organization’s website.

- Gaming: Most forms of gaming, if regularly carried on, are included in trade or business activities. Examples of this would be things like raffles, lotteries, pull-tabs, scratch-offs, parimutuel betting, Calcutta wagering, pickle jars, punchboards, tip boards, and so on. Bingo, however, is an exception.

- Rental Income: Rental income coming from renting out property on which there is a debt outstanding, may constitute unrelated debt-financed income. Or, income coming from personal services rendered in connection with the rental may be unrelated business taxable income.

- Parking Lots: If an organization operates a parking lot that is used by the general public, the parking fees would be taxable. And, if an organization enters into a lease with a third party who operates the organization’s parking lot, which the organization has a mortgage on, the renting fees paid to the organization are taxable.

Step Three: Determine the exceptions

There are some exceptions that are not subject to unrelated business income tax:

- Activities Conducted by Volunteers: If the trade or business activities are conducted for an organization by volunteers, the income produced is not subject to Unrelated Business Income Tax.

- Convenience: If trade or business activities are carried on by either a 501(c)(3) organization or a state college or university primarily for the convenience of its members, students, patients, officers, or employees, the income produced is not subject to Unrelated Business Income Tax

- Sale of Donated Merchandise: The income from selling merchandise that is substantially received as gifts or contributions is not subject to Unrelated Business Income Tax

- Distribution of Low-Cost Articles: The activities that are conducted by 501(c)(3) organizations and veterans’ organizations that involve the distribution of low-cost items in conjunction with the solicitation of charitable contributions, are not unrelated business activities.

- Convention or Trade Show: If one of the purposes of sponsoring activities, such as convention, annual meeting, or trade show, by a section 501(c)(3), (4), (5), or (6) organization is to promote the products or services of an industry or educate attendees of new industry developments, products, and services, and the organization regularly conducts such trade shows as one of its exempt purposes, these kinds of activities are not included in unrelated business activities.

- Sponsorship Payments: If a person pays an exempt organization only for the use or acknowledgement of the payer’s name, logo, or services or goods of insubstantial value. This is not included as income from unrelated business activities.

Step Four: Filing for Unrelated Business Income Tax (UBIT)

If a tax-exempt organization has gross unrelated business income more than $1,000 for any tax year, this exempt organization must file Form 990-T, in addition to the requirement to file Form 990, 990-EZ, 990-N, or 990-PF. Form 990-T is due the 15th day of the 5th month following the end of the organization’s accounting period (tax year). However, an automatic 6-month extension of time to file can be requested by filing Form 8868.

Failing to pay Unrelated Business Income Tax on time will lead to interest and penalty charges by IRS.

Forms that can be used to file UBIT:

| Form 990-T | Exempt Organization Business Income Tax Return |

| Form 990-W | Estimated Tax on Unrelated Business Taxable Income for Tax-Exempt Organizations |

| Form 1120 | U.S. Corporation Income Tax Return |

| Form 8868 | Application for Extension of Time to File Exempt Organization Return |

More information can be found in Publication 598, Tax on Unrelated Business Income of Exempt Organizations.

PROPERTY TAX EXEMPTIONS

Property tax is another tax that nonprofits still have to potentially pay. The qualification and application for property tax exemption varies in different states. To demonstrate what these differences can be, we share here a comparison of the California and Utah property tax codes (as of 2105). To understand your own state’s current tax code(s), visit their respective site using the state links above.

CALIFORNIA PROPERTY TAX EXEMPTION PROCESS

Step 1: Determine the eligibility of property tax exemption

In the State of California (as of the tax code of 2015) to apply for property tax exemption, a nonprofit organization must qualify under the tax-exempt regulations of the Internal Revenue Service 501(c)(3) or California Franchise Tax Board 23701(d).

In addition, to be eligible to apply for property tax exemption in the State of California, the nonprofit organization must be organized for one or more of the following tax exempt purposes: religious, hospital, scientific, or charitable. What’s more, the property claimed for tax exemption must be used exclusively for qualified exempt activity.

The property used by other organizations’ tax exempt organization (under Internal Revenue Code 501(c)(3) or 501(c)(4) or Franchise Tax Board 23701(d)), incidentally for exempt purposes only, can be a tax exemption.

Step 2: Apply for the property tax exemption

Firstly, the nonprofit organization should submit it’s formative documents, including:

- Current Articles of Incorporation filed with the Secretary of State

- Tax Letter from Internal Revenue Service or Franchise Tax Board

- Annual financial statements

- Documentation supporting exempt activity, to the Board of Equalization. If a nonprofit organization is eligible for property tax exemption, The Board of Equalization will issue an Organizational Clearance Certificate.

Secondly, the organization should apply at the local county assessor to have their property reviewed for qualifying use and to have the exemption issued.

Step 3: Filing

A retroactive filing is available for eligible organizations for up to 4 prior years, and maximum late-filing penalty for retroactive filing is $250 per year, per property.

Related Links

| Claim for Organizational Clearance Certificate | www.boe.ca.gov/proptaxes/pdf/boe277.pdf |

| Claim for Supplemental Clearance Certificate | www.boe.ca.gov/proptaxes/pdf/boe277l1.pdf |

| Assessors’ Handbook: AH267: Welfare, Church and Religious Exemptions | www.boe.ca.gov/proptaxes/pdf/ah267.pdf |

| County assessors and contact Information | www.boe.ca.gov/proptaxes/assessors.htm |

| Irrevocable Dedication and Dissolution language (Property Tax Rule 143) | www.boe.ca.gov/proptaxes/pdf/143Adopted.pdf |

| Publication 149 – Property Tax Welfare Exemption | www.boe.ca.gov/proptaxes/pdf/pub149.pdf |

| Welfare Exemption Claim forms and assessor information | www.boe.ca.gov/proptaxes/assessors.htm |

Related Forms

| BOE-262-AH | Church Exemption |

| BOE-263 | Lessors’ Exemption Claim |

| BOE-267-S | Religious Exemption Claim |

| BOE-267-SNT | Religious Exemption – Change in Eligibility or Termination Notice |

| BOE-277 | Claim for Organizational Clearance Certificate – Welfare Exemption |

| BOE-277-LLC | Claim for Organizational Clearance Certificate – Welfare Exemption – Limited Liability Company |

| BOE-278-OCC | Verification for Continued Eligibility of Organizational Clearance Certificate – Welfare Exemption or Veterans’ Organization Exemption |

| BOE-267 | Claim for Welfare Exemption (First Filing) |

| BOE-267-A | Claim for Welfare Exemption (Annual Filing) |

| BOE-267-H | Welfare Exemption Supplemental Affidavit, Housing – Elderly or Handicapped Families |

| BOE-267-L | Welfare Exemption Supplemental Affidavit, Housing – Lower-Income Households |

| BOE-267-R | Welfare Exemption Supplemental Affidavit, Rehabilitation – Living Quarters |

| BOE-277-F1 | Welfare or Veterans’ Organization Exemption Organizational Clearance Certificate |

| BOE-277-F2 | Welfare or Veterans’ Organization Exemption Organizational Clearance Certificate |

UTAH PROPERTY TAX EXEMPTION PROCESS

Step 1: Determine the eligibility of property tax exemption

Now let’s examine Utah. In the State of Utah (as of the tax code of 2015) property owned by a nonprofit organization which is used exclusively for religious, charitable and educational purpose, is exempt.

A partial exemption is granted only where a separately identifiable portion of a property is exclusively used for qualified purposes. For example, when part of a building is devoted to charitable purposes and part is rented out to individual private concerns for substantial consideration, only the part of the property that is used for charitable purposes is exempt from taxation, not the part of the building rented out for revenue. [Parker v. Quinn, (23 Utah 332)(64P 961), 1901] [Odd Fellows’ Bldg. Ass’n v. Naylor, 53 Utah 111, 177 P. 214 (1918)]

When a nonprofit entity acquires property after the lien date, and that property is to be used exclusively for religious, charitable, or educational purposes, it must collect and pay proportional property taxes from January 1st to the date of acquisition. (Section 59-2-1101)

If a property that is allowed the exclusive use exemption ceases to qualify for the exemption because of a change in ownership, the new owner is to pay a proportional tax based on the period of time beginning on the day that the new owner acquired the property and ending on the last day of the calendar year in which the property was acquired. [Section 59-2-1101 (4)]

When the property ceased to qualify for the exclusive use exemption because of an ownership change, the new owner and previous owner of the property are required to report the acquisition of the property to the county assessor within 30 days from the day that the new owner acquired the property. [Section 59-2-1101 (4)]

Step 2: Apply for the property tax exemption

A written application for exemption must be filed to the board of equalization as well as documents below:

- Description of the property

- Internal Revenue Service 501(c)(3) not-for-profit authorization

- Federal income tax returns for previous years

- All financial statements that reflect the use of the property, the source of all funds and the way they were expended including a list of all paid staff, how they are paid, and the nature of their services

- A description of use including percentage of time the property is used for various purposes and the degree that such purposes are carried out by volunteer staff

- Copies of leases or rental agreements for the property and descriptions of how the rents are determined

- A copy of the Articles of Incorporation, By-laws and other organizational information

Application documents for exemption must be filed by March 1. When a person acquires property on or after January 1 that qualifies for an exclusive use exemption, that person may apply for the exclusive use exemption on or before the later of: (1) March 1st or (2) 30 days after the day in which the property is acquired. [Section 59-2-1102 (10)]

Step 3: Filing

The owner of certain tax-exempt property is required to file a signed statement, no later than March 1st each year, certifying the use of the property during the past year.

Forms related

| PT-020 | Application for Property Tax Exemption |

| PT-020A | Application for Exemption Schedule A – Real Property |

| PT-020B | Application for Exemption Schedule B – Personal Property |

| PT-020C | Application for Exemption Schedule C – Benefactors |

| PT-021 | Annual Application and Statement for Continued Property Tax Exemption |

| PT-022 | Active Duty Armed Forces Property Tax Exemption Application |

| PT-023 | Application for Residential Property Exemption |

More forms information can be found at the link below:

http://propertytax.utah.gov/index.php/centrally-assessed-property

HOW TO SET YOURSELF UP TO BE TRANSPARENT

If the intent is to operate non-traditional nonprofit ventures (such as a teacher/demonstration community, village, or hub), maintaining transparency to prove your venture(s) as nonprofit is essential. Here we discuss the three foundations for accomplishing this:

If the intent is to operate non-traditional nonprofit ventures (such as a teacher/demonstration community, village, or hub), maintaining transparency to prove your venture(s) as nonprofit is essential. Here we discuss the three foundations for accomplishing this:

DISCLOSURE

Disclosure means transparency about how money is made and how it is spent. In the case of One Community, we will be disclosing quarterly/semi-annual/annual financial statements online and the proof of all monies going to the development and mission of One Community. Simply stated, if no distribution is made to the shareholders, the total revenue received from visitors (and all other revenue streams) minus the total expense (program service, utility, depreciation, marketing, taxes, etc.) should equal the amount of contribution to One Community. Sharing this information openly will ensure and prove to the public, the State Tax Department, and the Internal Revenue Service that One Community as a teacher/demonstration village and hub is a 501(c)(3) organization which deserves its tax exemptions.

BUSINESS MISSION

Your business mission should also demonstrate your nonprofit focus and purpose. As an example, One Community’s non-profit mission is transformational global change through designing, modeling, and open sourcing sustainably holistic, virally self-replicating, Highest Good of All solutions. These solutions are founded on comprehensive and modifiable village/city models that can be duplicated globally. Duplication can be accomplished both modularly and/or as complete teacher/demonstration hubs and include sustainable solutions for infrastructure, food, education, economics, fulfilled living, and more.

This mission and our global goals mean we fall under several different 501(c)(3) categories including “Education Organization” and “Low-income Housing Provider.” We are working to demonstrate and provide a living experience that is totally sustainable and educational as an open source model for replication as an environment, eco-tourism resort, and low-income housing option. This educational experience, environment, and the buildings and ongoing development process will be hosted by volunteer tutors living on site who maintain the environment, demonstrate how amazing it is to live in it, and share and continuously evolve all aspects of the open source sustainable components and model.

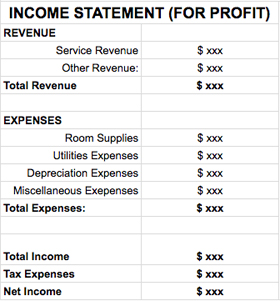

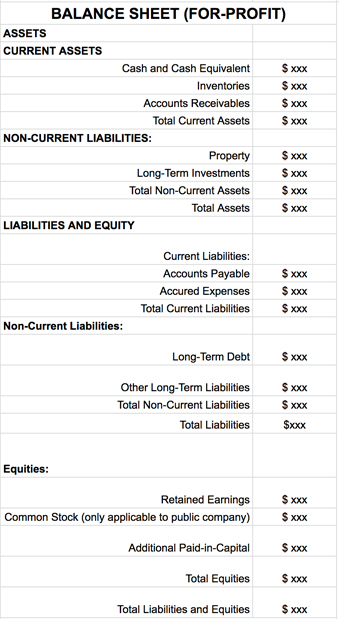

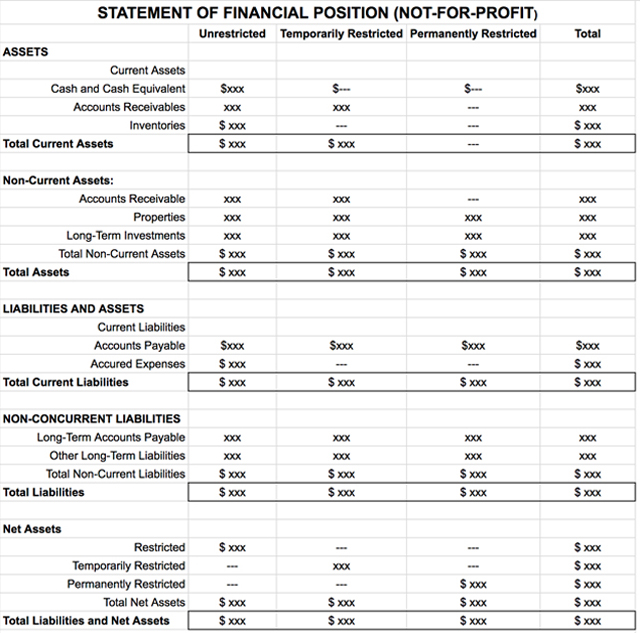

FINANCIAL REPORTING

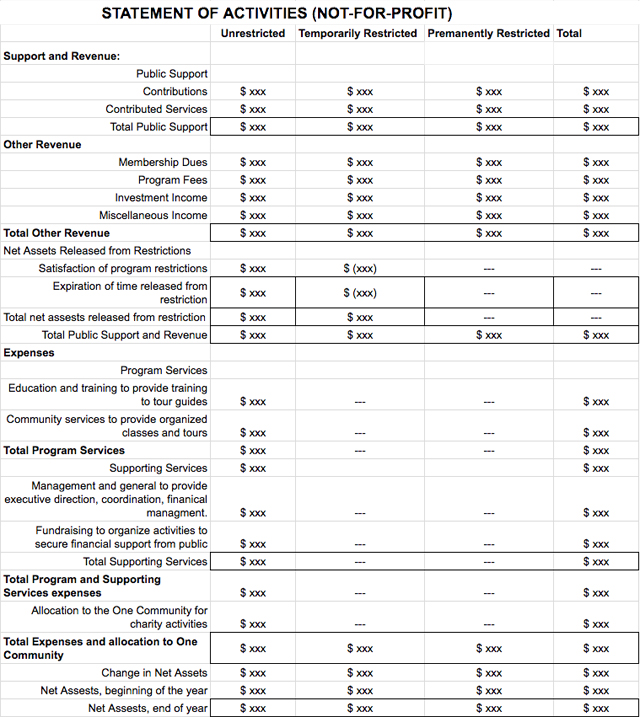

Last but arguably most important is your Financial Reporting. A certified financial statement should include two years of audited Balance Sheets and three years of audited Income Statements. Below examples show only a one-year format. They illustrate the income statement format for both the for-profit business and the not-for-profit organization.

NFP organizations account for their resources in different “funds,” and each of the funds is a separate accounting entity. This means the record of each fund is separate but there might be transfers between funds. According to the Financial Accounting Standards Board (FASB), NFP organizations must classify the net assets into three categories: Unrestricted, Temporarily Restricted, and Permanently Restricted. The classification of the assets is based on donors’ will, which means the person or corporation who made the contribution will decide the nature of the asset.

Generally, Permanently Restricted net assets are the endowments (income or form of property) with a principal (original sum) that can never be used, but the income from the principal is available for expenditure. Temporarily Restricted net assets are mainly the resources that are to be used for specific purposes in a set period of time. The net assets that do not fall into these two categories are Unrestricted Net Assets.

Contribution of services are the costs that would otherwise occur for the NFP if it is not performed by unpaid volunteers. Two criteria need to be met for a NFP to recognize a contribution of services:

- The services create or enhance non-financial assets

- The services require specialized skills and would likely need to be purchased if not donated

According to FASB, these services are those provided by accountants, carpenters, doctors, electricians, lawyers, nurses, plumbers, teachers, and other professionals. A journal entry for service contribution revenue would look something like this:

| Debit | Credit | |

| Expenses | $xxx | |

| Revenue from contributed services | $xxx |

Though GAAP allows organizations to recognize services revenue if the above two criteria are met, in the real world it is sometimes difficult to justify. Also, individuals cannot deduct the value of their time or services, so organizations should not issue receipts of donations for these services.

STATEMENT AND BALANCE SHEET EXAMPLES

For comparison, here are some income and balance statement examples for both for-profit and nonprofit entities. Depending on the nature of your organization, your statements may be simpler or more complex than these examples.

Here is a basic income statement for a for-profit entity:

Here is a basic balance sheet for a for-profit entity:

Now look at this basic financial assets statement for a not-for-profit entity:

Here is a basic revenue statement for a not-for-profit entity:

Here are examples of the Statement of Financial Position and Statement of Activities in a GoogleSpreadsheet you can copy. What should be obvious is that nonprofit statements require a much more detailed level of accounting because of their tax except benefits. That said, remember that each FP business or NFP organization will have differences in their financial reporting depending on the nature of the activities. So the above information is for illustration only, it does not cover all aspects of a business’ or NFP’s operations.

These examples were constructed with the accounts that will likely be used by One Community as an eco-tourism resort. For organizations with other products or services, the accounts needed can be very different. Here are some additional possible accounts for a Statement of Financial Position:

Assets:

- Charity gift annuity

- Beneficial interest in perpetual trust

- Contribution receivable from charitable remainder trust

- Notes receivable

- Leasehold improvements

- Deferred charges

- Others, these are just some of the more common ones

Liabilities:

- Accrued expenses

- Funds held for others

- Deposits

- Liabilities under interest-split agreement

- Bonds payable

- Government loan advances

- Others, these are just some of the more common ones

Here are some additional possible accounts for a Statement of Activities:

Revenue:

- Special events

- Special event incentives

- Legacies and bequests

- Allocated by federated fundraising organizations

- Grants from other organizations

- Other program fees (e.g. student tuitions, patient care charges, church service charges),

- Sale of necessary products (e.g. educational materials, prescribed medicines),

- Perpetual trust revenue

- Realized and unrealized gain on investment or properties

- Gain on investment transactions

- Others, these are just some of the more common ones

Expenses:

- Program services (e.g. employee salaries and benefits, research, public health education, professional training, inventories cost, scholarships to students),

- Supporting services (depreciation on buildings and equipment, investment management fees, change from retirement obligations, gains from discontinued operations),

- Allocations to other charity organizations, and etc.

- Others, these are just some of the more common ones

Again, the above accounts and classifications may vary based on specific organizations. For example, investment income might be within Program Services (the main function of an NFP organization) for a charity foundation, but Supporting Services for a hospital or college. It is important that organizations consult with a professional accountant who knows about your organization before setting up these accounts for yourself.

ONE COMMUNITY TAX SPECIFICS

This section will evolve to share the specifics of how we do our accounting for each of the One Community revenue streams. Once we are operating, we will include our actual cost and revenue sheets for all years of operation, open source editable spreadsheets, and any other specifics we feel are helpful or relevant.

HOME RENTAL/MANAGEMENT

When volunteers who have been a part of One Community long enough to have a home decide to leave the One Community property, they might want to let One Community manage their house during their leave and earn income from renting it out. When the volunteer (house owner) needs One Community to manage the house during their leave, the house owner will be charged for home maintenance expenses and receive profit when the house is rented out. At the same time, One Community will also earn revenue from providing the management service. We think this will be a win-win situation for both the home owner and One Community.

Here is a tutorial for how to record expenses and revenues in this case.

- Calculate the daily expense to maintain one house, including cleaning cost, toiletries expenses, utilities expenses, etc. For example, let’s say the total expense is $20 per day.

- When such expenses occur, debit the total amount to accounts receivable, credit cash / payable. One Community would not record expenses because the house is not owned or leased by One Community and the house owner is responsible for the maintaining cost of the house.

> Accounts receivable (from house owner) $20.00

> Cash/accounts payable $20.00 - If the house is not rented out during the house owner’s leave, no revenue is recognized. If the house is rented out, we would debit cash (or accounts receivable if customer pays by credit) and credit accounts payable to house owner. For example, imagine the daily charge for one room is $120 per day:

> Cash/accounts receivable $120.00

> Service revenue (for providing management service) $30.00

> Accounts payable (collected on behalf of house owner) $90.00 - Make the net payment ($90-$20=$70) to the house owners when they return.

> Accounts payable $90.00

> Accounts receivable $20.00

> Cash $70.00

Note: If the house owner wanted to make further contribution to One Community, then One Community would recognize this as contribution revenue and the donor would (in most circumstances) be able to deduct the amount.

OTHERS COMING

One Community will open source 100% of our revenue streams with complete details on how we manage each area, revenue, and the related tax details. This will include operating One Community as an eco-tourism destination, maintaining the entrepreneurial sponsorship details, and any other areas of revenue generation we engage.

RESOURCES

- One Community Resource: Revenue overview

- One Community Resource: Residency projections

- One Community Resource: Tourism revenue projections

- One Community Resource: For-profit open source economics hub

- One Community Resource: Non-profit open source economics hub

- One Community Resource: Business creation within One Community

- One Community Resource: Financial requirements for Pioneers Members of the team

- Use this page (click here) if you have a resource you’d like to suggest be added here

SUMMARY

Tourism revenue has been identified as the revenue stream most capable of accomplishing our global transformation goals by further supporting and sharing One Community as a teacher/demonstration community, village, and city. We will use a combination of the visitability of our location, educational classes, and non-stop creation of open source blueprints to market and share this option with the world. Sustainable infrastructure combined with an all volunteer labor force will keep operational expenses low while we share the fulfilled living and enriching environment as a marketable eco-tourism option. This will allow us to offer significantly more value, for a lower price, with an endless and free open source sharing marketing engine that benefits us and the world. In short, the more (and higher quality) our open source sharing, and the more fun our environment is, the more successful we will be; all of which will help to fuel our secondary revenue streams as well.

Tourism revenue has been identified as the revenue stream most capable of accomplishing our global transformation goals by further supporting and sharing One Community as a teacher/demonstration community, village, and city. We will use a combination of the visitability of our location, educational classes, and non-stop creation of open source blueprints to market and share this option with the world. Sustainable infrastructure combined with an all volunteer labor force will keep operational expenses low while we share the fulfilled living and enriching environment as a marketable eco-tourism option. This will allow us to offer significantly more value, for a lower price, with an endless and free open source sharing marketing engine that benefits us and the world. In short, the more (and higher quality) our open source sharing, and the more fun our environment is, the more successful we will be; all of which will help to fuel our secondary revenue streams as well.

FREQUENTLY ANSWERED QUESTIONS

Q: Is anyone (directors, consultants, etc.) paid as part of One Community?

No, we are a 100% unpaid volunteer organization.

Q: How would individuals who want to make money as part of One Community do so?

Please see our entrepreneurial model page.

Q: Are you basing these concepts on an existing model? In other words, how confident are you they will work?

These concepts are based on the foundations of intelligent business in almost any industry: providing value, low cost-to-profit ratio, and a quality marketing engine. The successful (and growing) model to compare what we are creating with would be the affordable tourism industry. Affordable tourism continues to gain market share and sustainability as an industry and an interest continue to grow also. Visiting a property like One Community’s, an environment like One Community’s, and hands on experience with all of One Community’s open source blueprints and creations all add to our desirability and marketability. Further add to this that the entire “staff” of One Community are non-profit volunteer residents not doing a “job,” but rather operating the Highest Good society model that is the core of One Community, makes it a fun place to be and visit, and an exciting and world changing organization to maintain.

Combining all these things produces: a place people want to visit, that will offer much more interesting and fun things to do, at a lower price, with a higher profit margin, staffed by people who are (instead of “workers”) equal and full shareholders in the experience. On top of this, we are changing the world for the better and the more fun and beautiful residents are able to make One Community, the more they individually benefit, the more visitors benefit, and the more it benefits One Community’s global transformation goals.

For these reasons, we are very confident in the financial viability of One Community.

Q: What about duplicability, how will this be duplicable for others?

The marketing engine of One Community is growing to specifically support and coordinate with other teacher/demonstration communities, villages, and cities too. When other teacher/demonstration hubs contribute to the global open source archive, we will help them promote their work through our engine. We will operate this like a franchise where inclusion is based on open source contributions to positive and permanent global transformation. This means future models will have a significantly easier time implementing this same model. We will are also be open source and free-sharing the complete for-profit, non-profit, and entrepreneurial model details of One Community so others will be able to duplicate them with or without association with One Community.

Q: Why have a for-profit component, why not be 100% non-profit?

As stated above, our belief now is that there won’t need to be a for-profit aspect of One Community. If some area of our project must be classified and taxed as for-profit venture, we will most likely operate and maintain it under a separate legal entity. We’ll still open source the complete details.

Q: If you are a team of people without debt, how do you intend to teach people with debt how to become free of debt?

Our goal is to clearly define as many of the variables as possible for creating a financially viable teacher/demonstration hub with a diversity of options for implementation to suit different demographics and budgets. The more One Community grows and expands, the more open source blueprints, tools, tutorials, and resources we will provide for others to duplicate our efforts. This is why we are focused on people joining the Pioneer Team that are financially stable, so we can focus 100% of our energy on open source creation for those that aren’t in such a fortunate position. This is also one of the reasons why we won’t move onto the property with any debt as an organization.

Q: If you are a non-profit organization, how do you intend to operate for-profit businesses too?

Any activities of One Community deemed by tax code and federal law to not be operable under our 501(c)3 status will be operated under a separate for-profit corporate entity.

Q: Will One Community ever pay any of its members?

One Community’s #1 financial priority is expansion and our global goals. If we are accomplishing expansion and these goals successfully, and a 100% consensus of the membership agrees that distribution of funds is tax compliant, aligned with our values, warranted, and will not in any way compromise these goals, then distributions can be made.

Q: What about property liability and ownership by individuals versus a foundation, corporation, etc.?

We researched Premise Liability and determined that the ownership form does not increase or decrease the total amount of liabilities taken by the owner or the manager, but it does influence the insurance coverage of the property. Only when the manager is also the owner of the property, can they insure the building and the office contents, otherwise the manager can only insure the office contents. (click here for a resource about this)

Regardless, the property owners or non-owner residents, are responsible for maintaining a relatively safe environment. When people enter the property and hurt themselves because the environment is not safe, they may sue the property owners or residents unless they are intoxicated or are trespassing. The residents are treated in the same manner as the property owner.

When insuring with this in mind, a business owner policy includes property coverage and general liability coverage. Property includes structures, their contents, etc. General liability insurance will insure against property damage or bodily injury suffered by a third party (not owned or employed by the business) accidentally caused by normal business operation. If the owner also occupies the property, the owner can insure the office building and the office contents of the building on the same policy. In the case of leased space, most insurance companies can only insure the office contents. (click her for a resource about this)

If the property manager is an employee of the property owner, the owner usually will continue to be liable for the injuries caused by negligence because employers are responsible for the action of their employees and agents. (click here for a resource about this)

![]()

Connect with One Community